Free G 45 Hawaii Template

Free G 45 Hawaii Template

The G 45 Hawaii form, officially known as the General Excise/Use Tax Return, is a critical document for businesses operating in Hawaii. This form is used to report general excise and use taxes, which are essential revenue sources for the state. It requires businesses to detail their income and applicable deductions or exemptions. Completing the G 45 accurately is imperative, as failing to do so can lead to disallowed exemptions and additional tax assessments. The form encompasses several sections, including a schedule for claiming various exemptions and deductions, which must be attached to the main return. Notably, the form distinguishes between different types of exemptions, such as those related to out-of-state sales, bad debts, and specific industry-related deductions. Additionally, it highlights that most ordinary business expenses are not deductible under this tax framework. Therefore, understanding the nuances of the G 45 is vital for compliance and financial planning for Hawaii-based businesses.

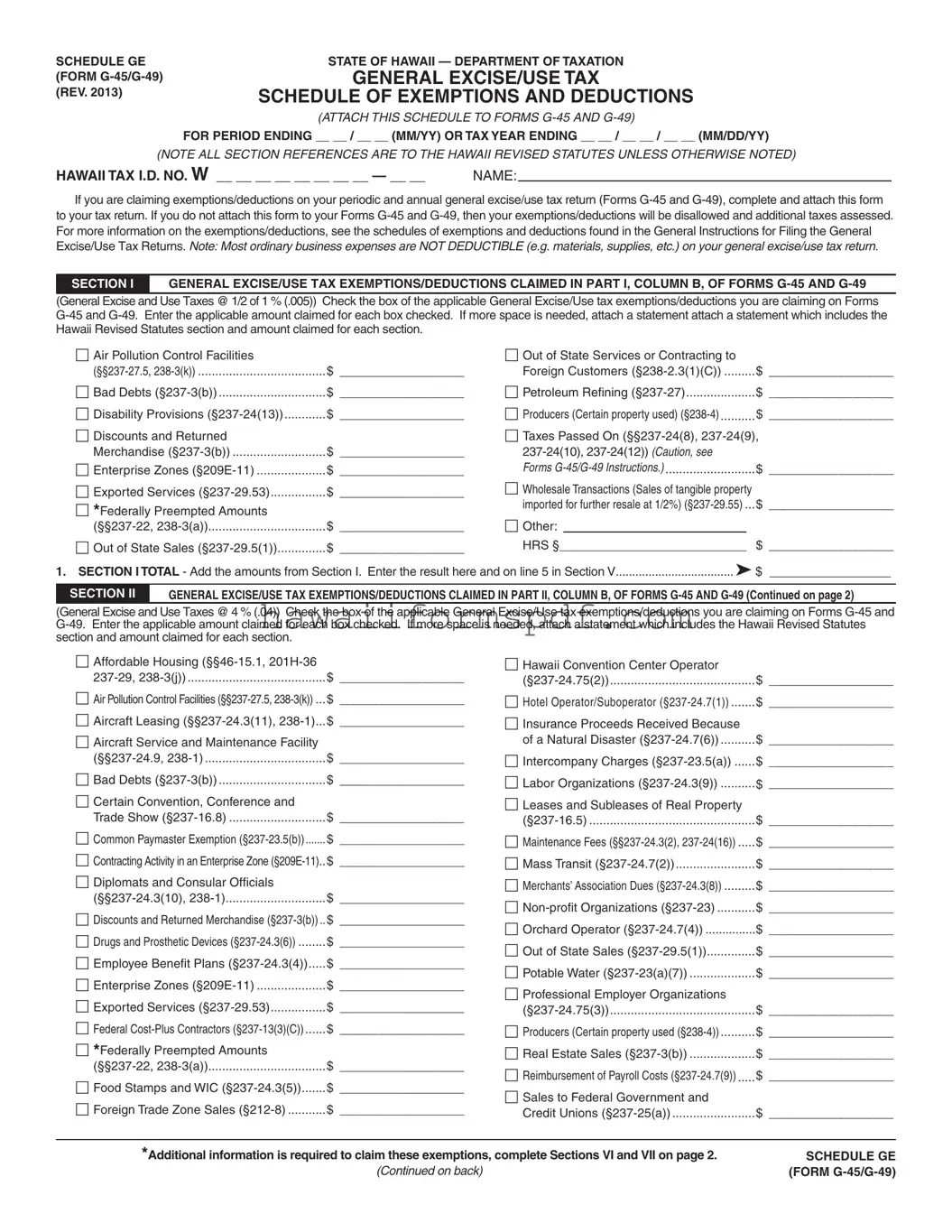

SCHEDULE GE |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

(FORM |

GENERAL EXCISE/USE TAX |

(REV. 2013) |

SCHEDULE OF EXEMPTIONS AND DEDUCTIONS |

|

|

|

(ATTACH THIS SCHEDULE TO FORMS |

|

FOR PERIOD ENDING __ __ / __ __ (MM/YY) OR TAX YEAR ENDING __ __ / __ __ / __ __ (MM/DD/YY) |

(NOTE ALL SECTION REFERENCES ARE TO THE HAWAII REVISED STATUTES UNLESS OTHERWISE NOTED)

HAWAII TAX I.D. NO. W __ __ __ __ __ __ __ __ — __ __ |

NAME: |

If you are claiming exemptions/deductions on your periodic and annual general excise/use tax return (Forms

SECTION I GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART I, COLUMN B, OF FORMS

(General Excise and Use Taxes @ 1/2 of 1 % (.005)) Check the box of the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms

Air Pollution Control Facilities |

|

Out of State Services or Contracting to |

|

|

|

|

||

$ __________________ |

Foreign Customers |

|

$ |

__________________ |

||||

Bad Debts |

$ __________________ |

Petroleum Refining |

|

$ |

__________________ |

|||

Disability Provisions |

$ __________________ |

Producers (Certain property used) |

|

$ |

__________________ |

|||

Discounts and Returned |

|

Taxes Passed On |

|

|||||

Merchandise |

$ __________________ |

|

|

|

|

|||

Enterprise Zones |

$ __________________ |

FORMS |

|

$ |

__________________ |

|||

Exported Services |

$ __________________ |

Wholesale Transactions (Sales of tangible property |

$ |

|

||||

*Federally Preempted Amounts |

|

imported for further resale at 1/2%) |

______________________ |

|||||

|

Other: |

|

|

|

|

|

||

$ __________________ |

|

|

|

|

|

|||

Out of State Sales |

$ __________________ |

HRS § |

|

|

|

$ |

__________________ |

|

|

|

|

||||||

1. SECTION I TOTAL - Add the amounts from Section I. Enter the result here and on line 5 in Section V |

$ |

__________________ |

||||||

SECTION II GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART II, COLUMN B, OF FORMS

(General Excise and Use Taxes @ 4 % (.04)) Check the box of the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms

Affordable Housing |

|

Hawaii Convention Center Operator |

|

|

|

$ __________________ |

$ |

__________________ |

|||

|

|

||||

Air Pollution Control Facilities |

$ ______________________ |

Hotel Operator/Suboperator |

$ |

______________________ |

|

Aircraft Leasing |

$ __________________ |

Insurance Proceeds Received Because |

|

|

|

Aircraft Service and Maintenance Facility |

|

of a Natural Disaster |

$ |

__________________ |

|

$ __________________ |

Intercompany Charges |

$ |

__________________ |

||

Bad Debts |

$ __________________ |

Labor Organizations |

$ |

__________________ |

|

Certain Convention, Conference and |

|

Leases and Subleases of Real Property |

|

|

|

Trade Show |

$ __________________ |

$ |

__________________ |

||

|

|

||||

Common Paymaster Exemption |

$ ______________________ |

Maintenance Fees |

$ |

______________________ |

|

Contracting Activity in an Enterprise Zone |

$ ______________________ |

Mass Transit |

$ |

__________________ |

|

Diplomats and Consular Officials |

|

Merchants’ Association Dues |

$ |

______________________ |

|

$ __________________ |

|

$ |

__________________ |

||

Discounts and Returned Merchandise |

$ ______________________ |

||||

Orchard Operator |

$ |

__________________ |

|||

Drugs and Prosthetic Devices |

$ __________________ |

||||

Out of State Sales |

$ |

__________________ |

|||

Employee Benefit Plans |

$ __________________ |

||||

Potable Water |

$ |

__________________ |

|||

Enterprise Zones |

$ __________________ |

||||

Professional Employer Organizations |

|

|

|||

Exported Services |

$ __________________ |

|

|

||

$ |

__________________ |

||||

Federal |

$ ______________________ |

Producers (Certain property used |

$ |

__________________ |

|

*Federally Preempted Amounts |

|

Real Estate Sales |

$ |

__________________ |

|

$ __________________ |

Reimbursement of Payroll Costs |

______________________ |

|||

Food Stamps and WIC |

$ __________________ |

||||

Sales to Federal Government and |

|

|

|||

Foreign Trade Zone Sales |

$ __________________ |

|

|

||

Credit Unions |

$ |

__________________ |

|||

|

|

|

|||

*Additional information is required to claim these exemptions, complete Sections VI and VII on page 2. |

|

SCHEDULE GE |

|||

|

(Continued on back) |

|

|

(FORM |

|

SCHEDULE GE (FORM

Name

PAGE 2

Hawaii Tax I.D. Number |

Period Ending (MM/YY) or |

|

Tax Year Ending (MM/DD/YY) |

|

|

SECTION II GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART II, COLUMN B, OF FORMS

Scientific Contracts |

$ __________________ |

*Subcontract Deduction |

$ |

__________________ |

||||

Services Related to Ships and Aircraft |

|

Sugar Cane Payments to Independent |

|

|

|

|||

$ __________________ |

Producers |

$ |

__________________ |

|||||

Shipbuilding and Ship Repairs |

$ __________________ |

Taxes Passed On |

|

|

|

|||

Shipping and Handling of Agricultural |

|

|

|

|||||

|

______________________ |

|||||||

Commodities |

$ __________________ |

|||||||

|

|

|

|

|

|

|||

Small Business Innovation Research |

|

TRICARE |

$ |

__________________ |

||||

|

Wholesale Amusements |

$ |

__________________ |

|||||

Grants |

$ __________________ |

|||||||

Stock Exchange Transactions |

Other: |

|

|

|

|

|||

|

|

|

|

|||||

|

|

HRS § |

|

|

$ |

__________________ |

||

2. SECTION II TOTAL - Add the amounts from Section II. Enter the result here and on line 6 in Section V |

$ |

__________________ |

||||||

SECTION III GENERAL EXCISE/USE TAX EXEMPTIONS/DEDUCTIONS CLAIMED IN PART III, COLUMN B, OF FORMS

(Insurance Commissions taxed @ .15% (.0015)) Check the box of the applicable General Excise/Use tax exemptions/deductions you are claiming on Forms

Bad Debts |

$ __________________ |

Other: |

|

|

|

|

|

||

|

|

|

HRS § |

|

|

$ |

__________________ |

||

3. SECTION III TOTAL - Add the amounts from Section III. Enter the result here and on line 7 in Section V |

$ |

__________________ |

|||||||

|

|

||||||||

SECTION IV |

COUNTY SURCHARGE EXEMPTIONS/DEDUCTIONS CLAIMED IN PART IV, COLUMN B, OF FORMS |

||||||||

(City and County of Honolulu Surcharge Tax @ 1/2 of 1% (.005)) Select the County Surcharge Tax exemptions/deductions that you are claiming. Enter the total amount claimed for each exemption/deduction.

|

Certain Contracts Entered into Before |

|

Subleases of Real Property |

$ |

__________________ |

||

|

6/30/2006 |

$ __________________ |

Wholesale Amusements |

$ |

__________________ |

||

|

Certain Oahu Sales |

|

|||||

|

$ __________________ |

|

|

|

|

||

4. |

SECTION IV TOTAL - Add the amounts from Section IV. Enter the result here and on line 8 in Section V |

$ |

__________________ |

||||

|

|

|

|

|

|

||

|

SECTION V |

TOTAL EXEMPTIONS/DEDUCTIONS CLAIMED ON FORMS |

|

|

|

||

5. |

Section I Total - Enter the amount from Section I, line 1 |

|

$ |

__________________ |

|||

6. |

Section II Total - Enter the amount from Section II, line 2 |

|

$ |

__________________ |

|||

7. |

Section III Total - Enter the amount from Section III, line 3 |

|

$ |

__________________ |

|||

8. |

Section IV Total - Enter the amount from Section IV, line 4 |

|

$ |

__________________ |

|||

9. |

GRAND TOTAL. Add lines 5 through 8 and enter the result on this line and on Form |

|

|

|

|||

|

or Form |

|

$ |

__________________ |

|||

|

|

|

|

|

|

||

|

SECTION VI |

ADDITIONAL INFORMATION REQUIRED FOR FEDERALLY PREEMPTED AMOUNTS CLAIMED |

|

|

|

||

If the amount claimed is exempt due to federal preemption, provide an explanation of the exemption and the federal statute (i.e., title and section of the United States Code) under which the exemption is being claimed (If more space is needed, attach a statement):

SECTION VII |

ADDITIONAL INFORMATION REQUIRED FOR SUBCONTRACT DEDUCTIONS AMOUNTS CLAIMED |

If you are claiming an deduction for payments made to a subcontractor or a specialty contractor, complete the required information below:

(If more space is needed, attach a statement. Include the total subcontract deductions claimed from any attachments in the total line below.)

SUBCONTRACTOR’S NAME AND/OR DBA NAME

SUBCONTRACTOR’S HAWAII TAX I.D. NO.

AMOUNT OF DEDUCTION

TOTAL SUBCONTRACT DEDUCTIONS CLAIMED |

$ |

*Additional information is required to claim these exemptions, complete Sections VI and VII.

SCHEDULE GE (Form

Filling out the G-45 Hawaii form requires careful attention to detail. This form is essential for claiming any exemptions or deductions related to your general excise and use taxes. Ensure you have all necessary information on hand before starting. Follow these steps to complete the form accurately.

After completing the form, review all entries for accuracy. Attach this schedule to your Forms G-45 and G-49 before submission. Missing this step could result in disallowance of your exemptions or deductions.

Filling out the G-45 Hawaii form can be a straightforward process, but many individuals and businesses make common mistakes that can lead to complications. Understanding these pitfalls can help ensure a smoother filing experience.

One frequent error is failing to attach the required Schedule GE. This schedule is essential for claiming exemptions and deductions. If it is not attached to Forms G-45 and G-49, the exemptions will be disallowed, resulting in additional taxes. Always double-check that this document is included before submission.

Another mistake is not checking the appropriate boxes for exemptions and deductions claimed. Each section has specific categories, and omitting a checkbox can lead to missing out on valid claims. It is crucial to carefully review each section to ensure all applicable boxes are marked.

Many people also forget to provide the correct amounts for each exemption or deduction. Each box checked must have a corresponding dollar amount filled in. Leaving these fields blank can delay processing and may lead to incorrect assessments.

Inaccurate or incomplete information about the Hawaii Tax I.D. number is another common issue. This number must be filled out correctly, as it identifies the taxpayer. Errors in this section can cause significant delays in processing and may require resubmission.

Some filers neglect to include additional information when claiming federally preempted amounts or subcontract deductions. Sections VI and VII require specific details and explanations. Failing to provide this information can lead to disallowance of these claims.

Additionally, misunderstanding the types of deductions available can lead to mistakes. For example, many ordinary business expenses are not deductible. It is essential to familiarize oneself with the exemptions and deductions outlined in the General Instructions for Filing to avoid claiming ineligible items.

Another common error involves not calculating totals accurately. Each section has a total that needs to be carried over to Section V. Miscalculations can result in discrepancies that may trigger audits or additional scrutiny from the Department of Taxation.

Some individuals also overlook deadlines for filing. It is important to be aware of the specific dates for submitting the G-45 and G-49 forms. Missing these deadlines can lead to penalties and interest charges.

Lastly, not keeping copies of submitted forms is a mistake that can have long-term consequences. Maintaining records of what has been filed is crucial for future reference and in case of any disputes or audits.

By being aware of these common mistakes, taxpayers can navigate the G-45 Hawaii form process more effectively. Taking the time to review and ensure accuracy can save time and prevent unnecessary complications down the road.

When navigating the tax landscape in Hawaii, especially regarding the General Excise Tax (GET), it's essential to be familiar with various forms and documents that complement the G-45 form. Understanding these documents can help ensure compliance and maximize any exemptions or deductions you may be eligible for. Below are some key forms often used alongside the G-45.

Being informed about these forms can significantly impact your business's financial health. Each document plays a unique role in ensuring that you comply with Hawaii's tax regulations while maximizing your eligible deductions and exemptions. Keep these forms in mind as you prepare your tax filings to navigate the process smoothly.

Hi W - The HW-14 outlines the financial responsibilities regarding employee wages.

For those looking to understand equine transactions, an essential document is the Horse Bill of Sale that outlines the terms of sale and protects both parties involved. For more information, visit this guide on Horse Bill of Sale forms.

Food Permit Hawaii - Coordinating with local event planners can aid in ensuring all necessary permits are accounted for.

Hawaii Harpta - It streamlines the process for property buyers in Hawaii.

The G-45 Hawaii form is used to report general excise and use taxes. Businesses in Hawaii must file this form periodically to report their earnings and claim any exemptions or deductions they qualify for. It helps ensure that businesses comply with state tax regulations while allowing them to reduce their tax liability through legitimate exemptions.

Any business operating in Hawaii that earns income subject to general excise tax must file the G-45 form. This includes sole proprietors, partnerships, corporations, and other entities engaged in trade or business activities. If your business has gross income, you are likely required to file this form, even if you have no tax due.

The G-45 form allows for various exemptions and deductions. Some common ones include:

It's important to check the specific sections of the form for a complete list and ensure you meet the eligibility requirements for each deduction.

If you fail to attach the G-45 form to your tax return, any exemptions or deductions you claim may be disallowed. This could result in additional taxes being assessed. It’s crucial to complete and attach the G-45 form to avoid penalties and ensure you’re only paying the taxes you owe.

To fill out the G-45 form correctly, carefully read the instructions provided with the form. Make sure you understand which exemptions and deductions apply to your business. If you have questions, consider consulting a tax professional who is familiar with Hawaii tax laws. Keeping accurate records and documentation will also help support your claims on the form.

| Fact Name | Details |

|---|---|

| Form Purpose | The G-45 form is used to report General Excise and Use Tax exemptions and deductions in Hawaii. |

| Governing Law | Hawaii Revised Statutes (HRS) §§237 and 238 govern the General Excise and Use Tax in Hawaii. |

| Filing Requirement | This form must be attached to Forms G-45 and G-49 to claim any exemptions or deductions. |

| Consequences of Non-compliance | If the G-45 form is not attached, claimed exemptions and deductions will be disallowed, resulting in additional taxes. |

| Exemption Types | Exemptions include those for bad debts, out-of-state services, and certain agricultural activities, among others. |

| Tax Rates | General Excise Tax rates vary, with specific rates noted for different types of transactions on the form. |

| Additional Information | Sections VI and VII require further details for federally preempted amounts and subcontract deductions. |

Understanding the G-45 form in Hawaii can be challenging, especially with the various misconceptions that often arise. Here are nine common misunderstandings regarding the G-45 form, along with clarifications to help you navigate the process more effectively.

This is not true. All businesses operating in Hawaii, regardless of size, are required to file the G-45 form if they are subject to general excise tax.

Many people believe that all business expenses are deductible. However, most ordinary business expenses, such as materials and supplies, are not deductible on the G-45 form.

Filing is mandatory even if you have no tax due. Failing to file can result in penalties and interest.

It is essential to attach the Schedule GE when claiming exemptions or deductions. If you do not, your claims may be disallowed.

Exemptions must be claimed and substantiated. If you fail to provide the necessary information or documentation, your exemptions may be denied.

While both forms are related to general excise tax, the G-45 is for periodic returns, and the G-49 is for annual returns. Each serves a different purpose.

There are specific deadlines for filing the G-45 form, usually on a monthly or quarterly basis, depending on your business's gross income.

Amending the G-45 is possible, but there are rules and time limits on how and when you can do so. It is crucial to follow the correct procedures.

Incorrect filings can lead to significant penalties and interest charges. It is vital to ensure that all information provided is accurate and complete.

By understanding these misconceptions, you can approach the G-45 form with greater confidence and ensure compliance with Hawaii's tax regulations.

When dealing with the G-45 Hawaii form, understanding its structure and requirements is crucial for accurate tax reporting. Here are some key takeaways:

By adhering to these guidelines, you can navigate the G-45 form more effectively and minimize the risk of errors that could lead to tax complications.