Free Hawaii Agreement Of Sale Template

Free Hawaii Agreement Of Sale Template

In the picturesque setting of Hawaii, the Agreement of Sale form serves as a vital document in real estate transactions, ensuring clarity and mutual understanding between buyers and sellers. This form outlines the essential terms of the sale, including the property description, sales price, and financing arrangements. It specifies what is included in the sale, from the property itself to any fixtures or appliances that may remain. Buyers and sellers alike must pay close attention to the details of the financing section, which can include various options such as cash sales, owner financing, or assumptions of existing loans. Additionally, the form emphasizes the importance of earnest money, a deposit made by the buyer to demonstrate commitment to the purchase. Property condition is another critical aspect, as it outlines the buyer's rights to inspect the property and the seller's obligations regarding repairs and disclosures. The closing process, title conveyance, and the allocation of closing costs are also meticulously detailed, ensuring that both parties are aware of their responsibilities. By understanding the components of the Hawaii Agreement of Sale form, participants can navigate the complexities of real estate transactions with greater confidence and ease.

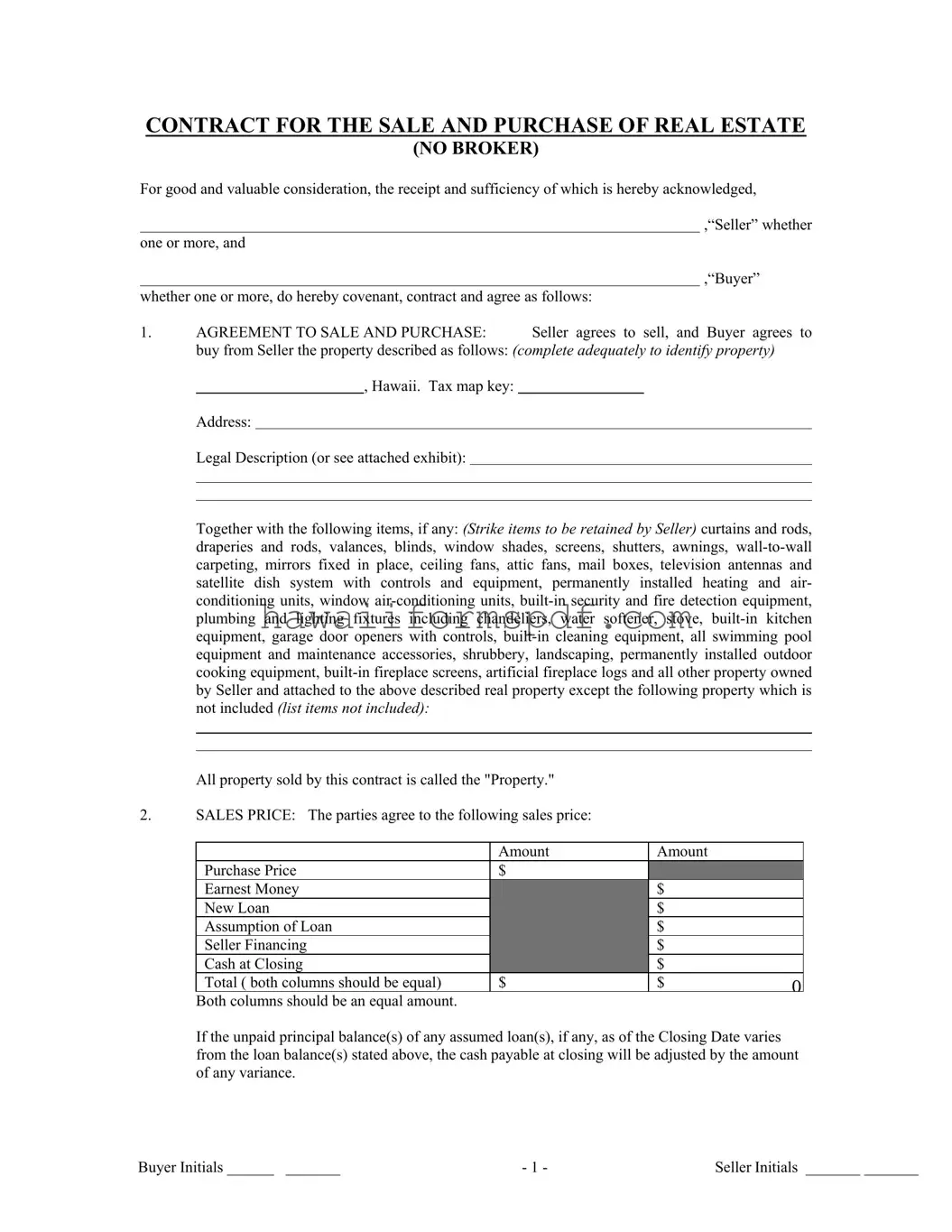

CONTRACT FOR THE SALE AND PURCHASE OF REAL ESTATE

(NO BROKER)

For good and valuable consideration, the receipt and sufficiency of which is hereby acknowledged,

|

|

|

,“Seller” whether |

one or more, and |

|

|

|

|

|

|

,“Buyer” |

whether one or more, do hereby covenant, contract and agree as follows: |

|||

1. |

AGREEMENT TO SALE AND PURCHASE: |

Seller agrees to sell, and Buyer agrees to |

|

buy from Seller the property described as follows: (complete adequately to identify property) , Hawaii. Tax map key:

Address:

Legal Description (or see attached exhibit):

Together with the following items, if any: (Strike items to be retained by Seller) curtains and rods, draperies and rods, valances, blinds, window shades, screens, shutters, awnings,

All property sold by this contract is called the "Property."

2.SALES PRICE: The parties agree to the following sales price:

|

Amount |

Amount |

|

Purchase Price |

$ |

|

|

Earnest Money |

|

$ |

|

New Loan |

|

$ |

|

Assumption of Loan |

|

$ |

|

Seller Financing |

|

$ |

|

Cash at Closing |

|

$ |

|

Total ( both columns should be equal) |

$ |

$ |

0 |

Both columns should be an equal amount. |

|

|

|

If the unpaid principal balance(s) of any assumed loan(s), if any, as of the Closing Date varies from the loan balance(s) stated above, the cash payable at closing will be adjusted by the amount of any variance.

Buyer Initials ______ _______ |

- 1 - |

Seller Initials _______ _______ |

3.FINANCING: The following provisions apply with respect to financing:

CASH SALE: This contract is not contingent on financing. |

|

|

|

|

|

|

||||||||

OWNER FINANCING: Seller agrees to finance |

|

|

|

|

|

|

dollars of the |

purchase |

||||||

price pursuant to a promissory note from Buyer to Seller of $ |

|

, bearing |

% |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

interest per annum, payable over a term of |

|

|

years |

with |

|

even monthly payments, |

||||||||

secured by a deed of trust or mortgage lien with the first payment to begin on the |

||||||||||||||

day of |

|

, 20 |

. |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NEW LOAN OR ASSUMPTION: This contract is contingent on Buyer obtaining

financing. Within days after the effective date of this contract Buyer shall apply for all financing or noteholder's approval of any assumption and make every reasonable effort to obtain financing or assumption approval. Financing or assumption approval will be deemed to have been obtained when the lender determines that Buyer has satisfied all of lender's financial requirements (those items relating to Buyer's net worth, income and creditworthiness). If financing or assumption approval is not obtained within

days after the effective date hereof, this contract will terminate and the earnest money will be refunded to Buyer. If Buyer intends to obtain a new loan, the loan will be of the following type:

Conventional

VA

FHA

Other:

The following provisions apply if a new loan is to be obtained:

FHA. It is expressly agreed that notwithstanding any other provisions of this contract, the Purchaser (Buyer) shall not be obligated to complete the purchase of the Property described herein or to incur any penalty by forfeiture of earnest money deposits or otherwise unless the Purchaser (Buyer) has been given in accordance with HUD/FHA or VA requirements a written statement by the Federal Housing Commissioner, Veterans Administration, or a Direct Endorsement lender setting forth the appraised value of the

Property of not less than $. The Purchaser (Buyer) shall have the privilege and option of proceeding with consummation of the contract without regard to the amount of the appraised valuation. The appraised valuation is arrived at to determine the maximum mortgage the Department of Housing and Urban Development will insure. HUD does not warrant the value nor the condition of the Property. The Purchaser (Buyer) should satisfy himself/herself that the price and condition of the Property are acceptable.

VA. If Buyer is to pay the purchase price by obtaining a new

Existing Loan Review. If an existing loan is not to be released at closing, Seller shall provide copies of the loan documents (including note, deed of trust or mortgage,

modifications) to Buyer within calendar days from acceptance of this contract. This contract is conditional upon Buyer's review and approval of the provisions of such loan documents. Buyer consents to the provisions of such loan documents if no written

objection is received by Seller from Buyer withincalendar days

from Buyer's receipt of such documents. If the lender's approval of a transfer of the Property is required, this contract is conditional upon Buyer's obtaining such approval

Buyer Initials ______ _______ |

- 2 - |

Seller Initials _______ _______ |

without change in the terms of such loan, except as may be agreed by Buyer. If

lender's approval is not obtained on or before ,

this contract shall be terminated on such date. The Seller

shall

shall

shall not, be released from liability under such existing loan. If Seller is to be released and release approval is not obtained, Seller may nevertheless elect to proceed to closing, or terminate this agreement in the sole discretion of Seller.

shall not, be released from liability under such existing loan. If Seller is to be released and release approval is not obtained, Seller may nevertheless elect to proceed to closing, or terminate this agreement in the sole discretion of Seller.

|

Credit Information. If Buyer is to pay all or part of the purchase price by executing a |

|||||||||||

|

promissory note in favor of Seller or if an existing loan is not to be released at closing, |

|||||||||||

|

this contract is conditional upon Seller's approval of Buyer's financial ability and |

|||||||||||

|

creditworthiness, which approval shall be at Seller's sole and absolute discretion. In such |

|||||||||||

|

case: (l) Buyer shall supply to Seller on or before |

|

, |

|

, |

at, |

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Buyer's expense, information and documents concerning Buyer's financial, employment |

|||||||||||

|

and credit condition; (2) Buyer consents that Seller may verify Buyer's financial ability |

|||||||||||

|

and creditworthiness; (3) any such information and documents received by Seller shall be |

|||||||||||

|

held by Seller in confidence, and not released to others except to protect Seller's interest |

|||||||||||

|

in this transaction; (4) if Seller does not provide written notice of Seller's disapproval to |

|||||||||||

|

Buyer on or before |

|

, |

|

|

|

, then Seller waives this |

|||||

|

condition. |

|

|

|

|

|

|

|

|

|

||

4. |

EARNEST MONEY: Buyer shall deposit $ |

|

|

|

|

as earnest money with |

|

|

|

|||

|

upon execution of this contract by both parties. |

|

|

|

|

|

|

|

|

|

||

5.PROPERTY CONDITION:

SELLER’S DISCLOSURE OF

is attached

is attached

is not applicable.

is not applicable.

Buyer hereby represents that he has personally inspected and examined the

Buyer accepts the property in its

Buyer may have the property inspected by persons of Buyer's choosing and at Buyer's expense. If the inspection report reveals defects in the property, Buyer shall notify Seller within 5 days of receipt of the report and may cancel this contract and receive a refund of earnest money, or close this agreement notwithstanding the defects, or Buyer and Seller may renegotiate this contract, in the discretion of Seller. All inspections and notices to Seller shall be complete

within days after execution of this agreement.

Buyer accepts the Property in its present condition; provided Seller, at Seller’s expense, shall complete the following repairs and treatment:

Buyer agrees that he will not hold Seller or its representatives responsible or liable for any present or future structural problems or damage to the foundation or slab of said property. If the subject residential dwelling was constructed prior to 1978, Buyer may conduct a risk assessment or inspection for the presence of

completed within days after execution of this agreement. In the alternative, Buyer may waive the opportunity to conduct an assessment/inspection by indicating said waiver on the attached

Buyer Initials ______ _______ |

- 3 - |

Seller Initials _______ _______ |

|

MECHANICAL EQUIPMENT AND BUILT IN APPLIANCES: All such equipment is sold |

|||||||||||||

|

shall be in good working order on the date of closing. Any |

|||||||||||||

|

repairs needed to mechanical equipment or appliances, if any, shall be the responsibility of |

|||||||||||||

|

Seller Buyer. |

|

|

|

|

|

|

|

|

|

|

|||

|

UTILITIES: Water is provided to the property by |

|

|

|

|

, |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sewer is provided by |

|

|

|

. Gas is provided by |

|

|

|

. |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Electricity is provided by |

|

|

. |

|

|

|

|

|

|||||

|

Other: |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|||||||

|

The present condition of all utilities is accepted by Buyer. |

|

|

|

|

|

||||||||

6. |

CLOSING: The closing of the sale will be on or before |

|

, 20 |

, unless |

||||||||||

|

extended pursuant to the terms hereof. |

|

|

|

|

|

|

|||||||

Closing may be extended to within 7 days after objections to matters disclosed in the title abstract, certificate or Commitment or by the survey have been cured.

If financing or assumption approval has been obtained, the Closing Date will be extended up to 15 days if necessary to comply with lender's closing requirements (for example, appraisal, survey, insurance policies,

7.TITLE AND CONVEYANCE: Seller is to convey title to Buyer by Warranty Deed or

(as appropriate) and provide Buyer with a Certificate of Title prepared by an attorney, title or abstract company upon whose Certificate or report title insurance may be obtained from a title insurance company qualified to do and doing business in the state of Hawaii. Seller will also execute a Bill of Sale, if necessary, for the transfer of any personal property. Seller shall, prior to or at closing, satisfy all outstanding mortgages, deeds of trust and special liens affecting the subject property which are not specifically assumed by Buyer herein. Title shall be good and marketable, subject only to (a) covenants, conditions and restrictions of record, (b) public, private utility easements and roads and

(e) general taxes for the year _______and subsequent years and (e) other:___________________. A title report shall be provided to Buyer at least 5 days prior to closing. If there are title defects, Seller shall notify Buyer within 5 days of closing and Buyer, at Buyer's option, may either (a) if defects cannot be cured by designated closing date, cancel this contract, in which case all earnest money deposited shall be returned, (b) accept title as is, or (c) if the defects are of such character that they can be remedied by legal action within a reasonable time, permit Seller such reasonable time to perform curative work at Seller's expense. In the event that the curative work is performed by Seller, the time specified herein for closing of this sale shall be extended for a reasonable period necessary for such action. Seller represents that the property may be legally used as zoned and that no government agency has served any notice to Seller requiring repairs, alterations or corrections of any existing condition except as stated herein.

8.APPRAISAL, SURVEY AND TERMITE INSPECTION: Any appraisal of the property shall be

the responsibility of Buyer |

Seller. A survey is: not required required, the cost of which |

|||

shall be paid by |

Seller |

Buyer. A termite inspection is not required |

required, the cost of |

|

which shall be paid by |

Seller |

Buyer. If a survey is required it shall be obtained within 5 days |

||

of closing. |

|

|

|

|

9.POSSESSION AND TITLE: Seller shall deliver possession of the Property to Buyer at closing.

Buyer Initials ______ _______ |

- 4 - |

Seller Initials _______ _______ |

Title shall be conveyed to Buyer, if more than one as |

Joint tenants with rights of survivorship, |

|||

tenants in common, |

Other: |

|

Prior to |

closing the property shall remain in the |

possession of Seller and Seller shall deliver the property to Buyer in substantially the same condition at closing, as on the date of this contract, reasonable wear and tear excepted.

10.CLOSING COSTS AND EXPENSES: The following closing costs shall be paid as provided. (Leave blank if the closing cost does not apply.)

|

Closing Costs |

|

Buyer |

|

|

Seller |

|

|

Both* |

|

|

|

|

|

|

|

|

||||

|

Attorney Fees |

|

|

|

|

|

|

|

|

|

|

Title Insurance |

|

|

|

|

|

|

|

|

|

|

Title Abstract or Certificate |

|

|

|

|

|

|

|

|

|

|

Property Insurance |

|

|

|

|

|

|

|

|

|

|

Recording Fees |

|

|

|

|

|

|

|

|

|

|

Appraisal |

|

|

|

|

|

|

|

|

|

|

Survey |

|

|

|

|

|

|

|

|

|

|

Termite Inspection |

|

|

|

|

|

|

|

|

|

|

Origination fees |

|

|

|

|

|

|

|

|

|

|

Discount Points |

|

|

|

|

|

|

|

|

|

|

If contingent on rezoning, cost and expenses of |

|

|

|

|

|

|

|

|

|

|

rezoning |

|

|

|

|

|

|

|

|

|

|

Other: |

|

|

|

|

|

|

|

|

|

All other closing costs

* 50/50 between buyer and seller.

11.PRORATIONS: Taxes for the current year, interest, maintenance fees, assessments, dues and rents, if any, will be prorated through the Closing Date. If taxes for the current year vary from the amount prorated at closing, the parties shall adjust the prorations when tax statements for the current year are available. If a loan is assumed and the lender maintains an escrow account, the escrow account must be transferred to Buyer without any deficiency. Buyer shall reimburse Seller for the amount in the transferred account. Buyer shall pay the premium for a new insurance policy. If taxes are not paid at or prior to closing, Buyer will be obligated to pay taxes for the current year.

12.CASUALTY LOSS: If any part of the Property is damaged or destroyed by fire or other casualty loss after the effective date of the contract, Seller shall restore the Property to its previous condition as soon as reasonably possible. If Seller fails to do so due to factors beyond Seller’s control, Buyer may either (a) terminate this contract and the earnest money will be refunded to Buyer, (b) extend the time for performance and the Closing Date will be extended as necessary, or

(c) accept the Property in its damaged condition and accept an assignment of insurance proceeds.

13.DEFAULT: If Buyer fails to comply with this contract, Buyer will be in default, and Seller may either (a) enforce specific performance, seek such other relief as may be provided by law, or both, or (b) terminate this contract and receive the earnest money as liquidated damages, thereby releasing both parties from this contract. If, due to factors beyond Seller’s control, Seller fails within the time allowed to make any

Buyer Initials ______ _______ |

- 5 - |

Seller Initials _______ _______ |

releasing both parties from this contract.

It is expressly understood and agreed that the failure of a party to insist in any one or more instances upon strict performance of any of the terms of this Agreement, or to exercise any rights herein conferred, shall not be deemed a waiver or relinquishment to any extent that party's rights to later assert or rely upon any such terms or rights in such instance and/or in any other instance.

14.ATTORNEY'S FEES: The prevailing party in any legal proceeding brought under or with respect to the transaction described in this contract is entitled to recover from the

15.REPRESENTATIONS: Seller represents that as of the Closing Date (a) there will be no liens, assessments, or security interests against the Property which will not be satisfied out of the sales proceeds unless securing payment of any loans assumed by Buyer and (b) assumed loans will not be in default. If any representation in this contract is untrue on the Closing Date, this contract may be terminated by Buyer and the earnest money will be refunded to Buyer. All representations contained in this contract will survive closing.

16.FEDERAL TAX REQUIREMENT: If Seller is a "foreign person", as defined by applicable law, or if Seller fails to deliver an affidavit that Seller is not a "foreign person", then Buyer shall withhold from the sales proceeds an amount sufficient to comply with applicable tax law and deliver the same to the Internal Revenue Service together with appropriate tax forms. IRS regulations require filing written reports if cash in excess of specified amounts is received in the transaction.

17.AGREEMENT OF PARTIES: This contract contains the entire agreement of the parties and cannot be changed except by their written agreement.

18.NOTICES: All notices from one party to the other must be in writing and are effective when mailed to,

To Buyer at: |

|

To Seller at: |

|

|

|

|

|

|

|

|

|

Telephone ( )

Facsimile ( )

Telephone ( )

Facsimile ( )

19.ASSIGNMENT: This agreement may not be assigned by Buyer without the consent of Seller. This agreement may be assigned by Seller and shall be binding on the heirs and assigns of the parties hereto.

20.PRIOR AGREEMENTS: This contract incorporates all prior agreements between the parties, contains the entire and final agreement of the parties, and cannot be changed except by their written consent. Neither party has relied upon any statement or representation made by the other party or any sales representative bringing the parties together. Neither party shall be bound by any terms, conditions, oral statements, warranties, or representations not herein contained. Each party acknowledges that he has read and understands this contract. The provisions of this contract shall apply to and bind the heirs, executors, administrators, successors and assigns of the respective parties hereto. When herein used, the singular includes the plural and the masculine includes the feminine as the context may require.

Buyer Initials ______ _______ |

- 6 - |

Seller Initials _______ _______ |

21.NO BROKER OR AGENTS: The parties represent that neither party has employed the services of a real estate broker or agent in connection with the property, or that if such agents have been employed, that the party employing said agent shall pay any and all expenses outside the closing of this agreement.

22.EMINENT DOMAIN: If the property is condemned by eminent domain after the effective date

hereof, the Seller and Buyer shall agree to continue the closing, or a portion thereof, or cancel this Contract. If the parties cannot agree, this contract shall

remain valid with Buyer being entitled to any condemnation proceeds at or after closing, or

remain valid with Buyer being entitled to any condemnation proceeds at or after closing, or

be cancelled and the earnest money returned to Buyer.

be cancelled and the earnest money returned to Buyer.

23.OTHER PROVISIONS

24.TIME IS OF THE ESSENCE IN THE PERFORMANCE OF THIS AGREEMENT.

25.GOVERNING LAW: This contract shall be governed by the laws of the State of Hawaii.

26.DEADLINE LIST (Optional) (complete all that apply). Based on other provisions of Contract.

Deadline

Loan Application Deadline, if contingent on loan

Loan Commitment Deadline

Buyer(s) Credit Information to Seller

Disapproval of Buyers Credit Deadline

Survey Deadline

Title Objection Deadline

Survey Deadline

Appraisal Deadline

Property Inspection Deadline

Date

Whether or not listed above, deadlines contained in this Contract may be extended informally by a writing signed by the person granting the extension except for the closing date which must be extended by a writing signed by both Seller and Buyer.

EXECUTED the |

|

day of |

|

, 20 |

(THE EFFECTIVE DATE). |

|||

|

|

|

|

|

|

|

|

|

|

Buyer |

|

|

|

|

Seller |

|

|

|

|

|

|

|

|

|

|

|

|

Buyer |

|

|

|

|

Seller |

|

|

Buyer Initials ______ _______ |

- 7 - |

Seller Initials _______ _______ |

EXHIBIT FOR DESCRIPTION OR ATTACH SEPARATE DESCRIPTION

Buyer Initials ______ _______ |

- 8 - |

Seller Initials _______ _______ |

|

|

|

|

RECEIPT |

|

|

|

|

|

||||

Receipt of Earnest Money is acknowledged. |

|

|

|

|

|

||||||||

Signature: |

|

|

Date: |

, 20 |

|||||||||

By: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Telephone ( |

) |

|

|

|

||||

Address |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

Facsimile ( |

) |

|

|

|

||||

City |

State |

Zip Code |

|

|

|

|

|

|

|

||||

Buyer Initials ______ _______ |

- 9 - |

Seller Initials _______ _______ |

Completing the Hawaii Agreement of Sale form is a critical step in the real estate transaction process. By following these steps carefully, you can ensure that all necessary information is accurately captured, paving the way for a smooth transaction. Here’s how to fill out the form:

After filling out the form, review all entries for accuracy. It’s essential that both parties understand the terms outlined and agree to them before moving forward. This form will serve as a binding agreement, so clarity and precision are paramount.

Filling out the Hawaii Agreement of Sale form can be a daunting task, and mistakes can easily occur. One common error is failing to adequately identify the property being sold. The form requires specific details such as the tax map key, address, and legal description. If any of these details are missing or incorrect, it could lead to confusion and complications later in the transaction.

Another frequent mistake involves the sales price section. Buyers and sellers must ensure that both columns for the purchase price and earnest money are equal. A simple arithmetic error could result in misunderstandings or disputes. It is essential to double-check these figures to avoid any discrepancies that could complicate the closing process.

Moreover, many individuals overlook the financing provisions. Whether the sale is contingent on financing or involves owner financing, it is crucial to fill out these sections accurately. Failing to specify the type of financing or the terms can lead to significant issues down the line, especially if the buyer is unable to secure the necessary funds.

Buyers often neglect the importance of the property condition clause. The form states that the buyer accepts the property in its "as-is" condition, but it also allows for inspections. Buyers should be aware of their rights to conduct inspections and notify the seller of any defects. Ignoring this step can lead to unexpected repairs and costs after the sale is finalized.

Another common oversight is related to the earnest money deposit. Buyers must ensure that they deposit the correct amount with the appropriate party upon executing the contract. Not doing so could jeopardize the entire agreement. Additionally, the timeline for submitting this deposit should be closely followed to avoid any potential breaches of contract.

People often misinterpret the closing date provisions. The contract specifies that the closing should occur by a certain date unless extended. If either party fails to meet this deadline, it is essential to understand the consequences and remedies available. A lack of clarity here can lead to confusion and disputes regarding the closing process.

Furthermore, buyers frequently overlook the necessity of reviewing existing loan documents if applicable. If the seller has an existing loan that is not to be released at closing, the buyer should carefully review these documents to ensure they understand any obligations or restrictions. Failing to do so can lead to unexpected liabilities for the buyer.

Lastly, individuals often forget to address closing costs and expenses. The form provides a section for detailing who is responsible for various closing costs. It is important to clearly outline these responsibilities to avoid misunderstandings at closing. If not addressed, disputes over who pays what can arise, potentially delaying the transaction.

The Hawaii Agreement of Sale form is a crucial document in the real estate transaction process, but it often goes hand in hand with several other important forms and documents. Each of these documents serves a specific purpose and helps ensure that both the buyer and seller are protected throughout the transaction. Below is a list of commonly used forms and documents that complement the Hawaii Agreement of Sale.

Understanding these documents is essential for anyone involved in a real estate transaction in Hawaii. Each form plays a vital role in ensuring a smooth process and protecting the interests of both buyers and sellers. Being informed can help you navigate the complexities of real estate transactions with confidence.

Hawaii Llc Cost - The X-8 form is necessary for compliance with the Hawaii Revised Statutes.

In order to complete the necessary documentation for vehicle transactions in Texas, it is highly recommended to use the Texas Documents, which provides a reliable version of the Statement of Fact Texas form, ensuring that all required information is collected accurately and effectively.

Trademark Search Hawaii - The T 4 form outlines specific classifications for different types of trademarks or service marks.

The Hawaii Agreement of Sale form is a legal document used in real estate transactions in Hawaii. It outlines the terms and conditions under which a seller agrees to sell property to a buyer. This form is specifically for transactions without a broker involved, ensuring that both parties understand their obligations and rights throughout the sale process.

To complete the Hawaii Agreement of Sale form, the following information is necessary:

Earnest money is a deposit made by the buyer to demonstrate their commitment to purchasing the property. In the Hawaii Agreement of Sale form, the buyer is required to deposit a specified amount as earnest money upon execution of the contract. This amount is typically held in escrow and will be applied toward the purchase price at closing. If the transaction does not proceed as agreed, the handling of the earnest money will depend on the circumstances outlined in the contract.

If the buyer is unable to secure financing within the specified timeframe, the contract will terminate. In such cases, the earnest money will be refunded to the buyer. It is essential for the buyer to apply for financing promptly and make every reasonable effort to obtain approval to avoid this situation.

Yes, the seller is required to disclose any known issues with the property, particularly regarding lead-based paint hazards if the property was built before 1978. This disclosure is mandated by federal law and must be included as an addendum to the agreement.

The property condition clause in the Hawaii Agreement of Sale form states that the buyer accepts the property in its "as-is" condition. The buyer has the right to conduct inspections at their own expense. If any significant defects are discovered, the buyer can notify the seller and choose to cancel the contract, close despite the defects, or negotiate repairs.

Closing costs are outlined in the Hawaii Agreement of Sale form and can include various fees such as attorney fees, title insurance, appraisal costs, and recording fees. The agreement specifies which party is responsible for each cost. In some cases, costs may be split between the buyer and seller.

If the property is damaged by fire or another casualty after the contract is effective, the seller is responsible for restoring the property to its previous condition. If the seller fails to do so, the buyer has several options: terminate the contract for a refund of earnest money, extend the closing date, or accept the property in its damaged state along with any insurance proceeds.

The seller must convey title to the buyer using a Warranty Deed, ensuring that the title is good and marketable. The seller is also responsible for satisfying any outstanding mortgages or liens on the property before closing. A title report must be provided to the buyer at least five days prior to closing, allowing the buyer to review for any defects.

If either party defaults on the agreement, the non-defaulting party has specific remedies available. For the buyer, this may include enforcing specific performance or terminating the contract and recovering earnest money. For the seller, if they fail to meet their obligations, the buyer may choose to extend the performance time or terminate the contract and receive their earnest money back.

| Fact Name | Details |

|---|---|

| Purpose | The Hawaii Agreement of Sale form is used for the sale and purchase of real estate without the involvement of a broker. |

| Governing Law | This form is governed by the laws of the State of Hawaii, specifically under Hawaii Revised Statutes relating to real property transactions. |

| Earnest Money | The Buyer is required to deposit earnest money upon execution of the contract, which shows their commitment to the purchase. |

| Property Condition | Buyers accept the property in its "as-is" condition, meaning they take responsibility for any issues discovered after the sale. |

Here are nine common misconceptions about the Hawaii Agreement of Sale form:

This form can be used for various types of real estate transactions, not just residential properties. It applies to any real estate sale in Hawaii.

Earnest money can be refunded under certain conditions, such as if financing is not approved or if the buyer cancels the contract due to property defects.

Buyers have the right to inspect the property and can cancel the contract if significant defects are found.

Buyers accept the property "as-is," but sellers may still be required to complete specific repairs if agreed upon in the contract.

The closing date can be extended under certain conditions, such as issues with financing or title defects.

Closing costs can be split between buyers and sellers, as outlined in the agreement.

The contract may be contingent on financing, meaning buyers must secure a loan for the purchase to proceed.

Sellers must fulfill certain obligations, such as providing clear title and making necessary repairs, as specified in the contract.

Buyers are encouraged to obtain an appraisal, especially if financing is involved, to ensure the property's value meets or exceeds the purchase price.

Filling out and using the Hawaii Agreement of Sale form requires careful attention to detail. Here are some key takeaways to keep in mind: