Free Hawaii M 38 Template

Free Hawaii M 38 Template

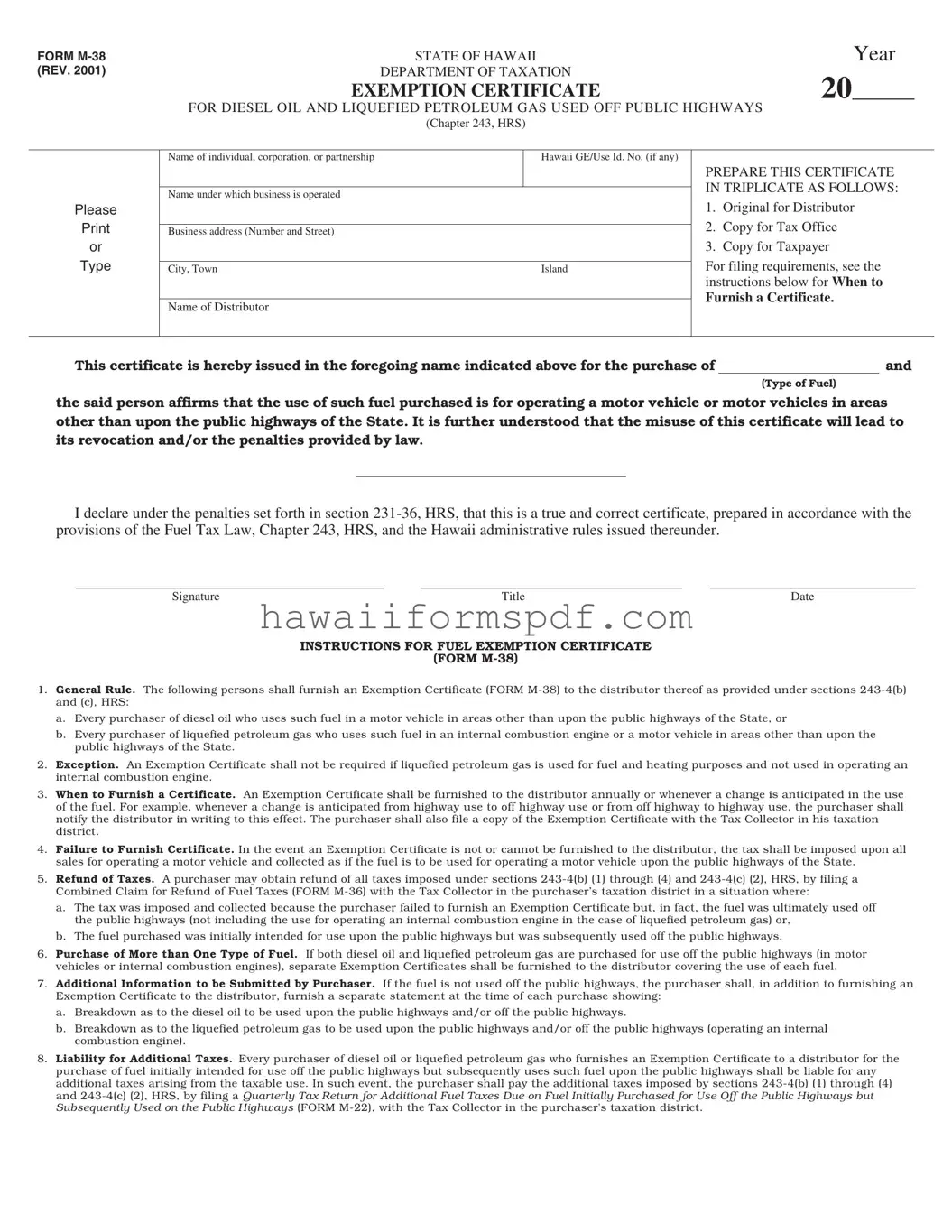

The Hawaii M 38 form serves as a crucial document for individuals and businesses utilizing diesel oil and liquefied petroleum gas (LPG) in ways that do not involve public highways. This form, officially known as the Exemption Certificate for Diesel Oil and Liquefied Petroleum Gas Used Off Public Highways, is designed to facilitate tax exemptions for fuel used in motor vehicles or internal combustion engines in off-highway applications. When filling out this form, users must provide essential information, including the name of the purchaser, the type of fuel being purchased, and the name of the distributor. This certificate must be prepared in triplicate: one copy for the distributor, one for the tax office, and one for the taxpayer's records. Importantly, the form emphasizes the responsibility of the purchaser to affirm that the fuel will be used off public highways, as misuse can lead to penalties or revocation of the certificate. Additionally, the Hawaii Department of Taxation outlines specific instructions regarding when to furnish this certificate, the potential for tax refunds, and the consequences of failing to provide it. Understanding these aspects is vital for compliance and to avoid unnecessary tax liabilities. Whether for a small business or a large corporation, the Hawaii M 38 form plays a significant role in managing fuel taxes effectively.

FORM |

|

STATE OF HAWAII |

|

|

Year |

|

||

(REV. 2001) |

|

DEPARTMENT OF TAXATION |

|

20 |

|

|

|

|

|

EXEMPTION CERTIFICATE |

|

|

|

|

|||

|

FOR DIESEL OIL AND LIQUEFIED PETROLEUM GAS USED OFF PUBLIC HIGHWAYS |

|

||||||

|

|

(Chapter 243, HRS) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of individual, corporation, or partnership |

|

Hawaii GE/Use Id. No. (if any) |

|

|

|

|

|

|

|

|

|

PREPARE THIS CERTIFICATE |

|

|||

|

|

|

|

IN TRIPLICATE AS FOLLOWS: |

|

|||

|

Name under which business is operated |

|

|

|

||||

|

|

|

|

|

|

|

|

|

Please |

|

|

|

1. |

Original for Distributor |

|

||

|

|

|

2. Copy for Tax Office |

|

||||

Business address (Number and Street) |

|

|

|

|||||

or |

|

|

|

3. Copy for Taxpayer |

|

|||

Type |

|

|

|

For filing requirements, see the |

|

|||

City, Town |

|

Island |

|

|||||

|

|

|

|

instructions below for WHEN TO |

|

|||

|

|

|

|

FURNISH A CERTIFICATE. |

|

|||

|

Name of Distributor |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This certificate is hereby issued in the foregoing name indicated above for the purchase of |

|

|

and |

|

||||

|

|

|

|

|

(Type of Fuel) |

|

||

the said person affirms that the use of such fuel purchased is for operating a motor vehicle or motor vehicles in areas other than upon the public highways of the State. It is further understood that the misuse of this certificate will lead to its revocation and/or the penalties provided by law.

I declare under the penalties set forth in section

Signature |

Title |

Date |

INSTRUCTIONS FOR FUEL EXEMPTION CERTIFICATE

(FORM

1.General Rule. The following persons shall furnish an Exemption Certificate (FORM

a.Every purchaser of diesel oil who uses such fuel in a motor vehicle in areas other than upon the public highways of the State, or

b.Every purchaser of liquefied petroleum gas who uses such fuel in an internal combustion engine or a motor vehicle in areas other than upon the public highways of the State.

2.Exception. An Exemption Certificate shall not be required if liquefied petroleum gas is used for fuel and heating purposes and not used in operating an internal combustion engine.

3.When to Furnish a Certificate. An Exemption Certificate shall be furnished to the distributor annually or whenever a change is anticipated in the use of the fuel. For example, whenever a change is anticipated from highway use to off highway use or from off highway to highway use, the purchaser shall notify the distributor in writing to this effect. The purchaser shall also file a copy of the Exemption Certificate with the Tax Collector in his taxation district.

4.Failure to Furnish Certificate. In the event an Exemption Certificate is not or cannot be furnished to the distributor, the tax shall be imposed upon all sales for operating a motor vehicle and collected as if the fuel is to be used for operating a motor vehicle upon the public highways of the State.

5.Refund of Taxes. A purchaser may obtain refund of all taxes imposed under sections

a.The tax was imposed and collected because the purchaser failed to furnish an Exemption Certificate but, in fact, the fuel was ultimately used off the public highways (not including the use for operating an internal combustion engine in the case of liquefied petroleum gas) or,

b.The fuel purchased was initially intended for use upon the public highways but was subsequently used off the public highways.

6.Purchase of More than One Type of Fuel. If both diesel oil and liquefied petroleum gas are purchased for use off the public highways (in motor vehicles or internal combustion engines), separate Exemption Certificates shall be furnished to the distributor covering the use of each fuel.

7.Additional Information to be Submitted by Purchaser. If the fuel is not used off the public highways, the purchaser shall, in addition to furnishing an Exemption Certificate to the distributor, furnish a separate statement at the time of each purchase showing:

a.Breakdown as to the diesel oil to be used upon the public highways and/or off the public highways.

b.Breakdown as to the liquefied petroleum gas to be used upon the public highways and/or off the public highways (operating an internal combustion engine).

8.Liability for Additional Taxes. Every purchaser of diesel oil or liquefied petroleum gas who furnishes an Exemption Certificate to a distributor for the purchase of fuel initially intended for use off the public highways but subsequently uses such fuel upon the public highways shall be liable for any additional taxes arising from the taxable use. In such event, the purchaser shall pay the additional taxes imposed by sections

Completing the Hawaii M-38 form is essential for those purchasing diesel oil or liquefied petroleum gas for use off public highways. This process ensures compliance with state regulations regarding fuel use. The form must be filled out accurately to avoid penalties and to facilitate the proper handling of fuel tax exemptions.

Filling out the Hawaii M-38 form can seem straightforward, but there are common mistakes that can lead to complications. One frequent error is neglecting to provide the correct Hawaii GE/Use Id. No. If you have one, it is crucial to include it. This number helps the tax authorities identify your business and ensures that your exemption is processed correctly. Omitting this information can delay your application and may lead to additional tax liabilities.

Another common mistake is failing to sign the form. The signature is not just a formality; it serves as a declaration that the information provided is accurate and truthful. Without a signature, the form is considered incomplete, and you may face penalties. Take the time to review the form and ensure that all required signatures are in place before submission.

In addition, some individuals mistakenly use the form for purposes other than those intended. The M-38 form is specifically for diesel oil and liquefied petroleum gas used off public highways. If the fuel is used for heating or other purposes, a different form may be required. Misusing the form can lead to revocation of your exemption and financial penalties.

Another area where mistakes often occur is in the description of the fuel type. It is essential to clearly specify whether you are purchasing diesel oil or liquefied petroleum gas. If you are purchasing both, separate certificates are necessary for each type of fuel. Failing to differentiate between the two can result in complications when filing your taxes and might even lead to a denial of your exemption.

Lastly, many people overlook the requirement to notify the distributor of any changes in fuel use. If your intended use changes from off-highway to on-highway or vice versa, you must inform the distributor in writing. Not doing so can result in unexpected tax liabilities. Keeping accurate records and being proactive about changes can save you time and money in the long run.

The Hawaii M-38 form is essential for those purchasing diesel oil and liquefied petroleum gas for use off public highways. However, several other forms and documents are often used alongside it to ensure compliance with state regulations. Here’s a brief overview of those documents.

Understanding these forms and their purposes can help ensure that you remain compliant with Hawaii's tax regulations regarding fuel usage. Proper documentation not only helps avoid penalties but also facilitates smoother transactions with fuel distributors.

Maui Get Tax Rate - The form facilitates the calculation of taxes owed for various business activities.

When navigating the world of equine transactions, utilizing a well-structured Horse Bill of Sale template can simplify the process and ensure accuracy. For those seeking clarity in horse ownership transfers, this important form is essential for formalizing such agreements in Colorado. For more information, you can visit the necessary Horse Bill of Sale document.

Boh Routing Number - Only retirees or beneficiaries can initiate this direct deposit agreement.

The Hawaii M-38 form is an Exemption Certificate for diesel oil and liquefied petroleum gas used off public highways. This form is issued by the State of Hawaii's Department of Taxation and is necessary for individuals, corporations, or partnerships purchasing these fuels for purposes other than operating vehicles on public highways.

Any purchaser of diesel oil or liquefied petroleum gas who intends to use the fuel in a motor vehicle or internal combustion engine in areas other than public highways must complete the M-38 form. This includes businesses and individuals who will use these fuels off-road or in non-highway applications.

The M-38 form should be furnished to the distributor annually or whenever there is a change in the intended use of the fuel. For instance, if a purchaser shifts from using fuel on public highways to using it off-road, they must notify the distributor in writing and submit the M-38 form accordingly.

If a purchaser fails to provide the M-38 form to the distributor, the tax will be imposed on all fuel sales as if the fuel were being used on public highways. This means that the purchaser may end up paying higher taxes than necessary if the fuel is actually used off-road.

Yes, a purchaser may obtain a refund of taxes if they can demonstrate that the fuel was ultimately used off public highways, despite not having submitted the M-38 form initially. To do this, they must file a Combined Claim for Refund of Fuel Taxes (FORM M-36) with the Tax Collector in their taxation district.

Yes, if you are purchasing both diesel oil and liquefied petroleum gas for off-highway use, you must provide separate M-38 forms for each type of fuel. This ensures that the distributor has the correct documentation for both fuel types.

If the fuel is not used off public highways, the purchaser must provide a separate statement at the time of each purchase. This statement should include a breakdown of the diesel oil and liquefied petroleum gas intended for use on public highways versus off public highways.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Hawaii M-38 form is an Exemption Certificate for diesel oil and liquefied petroleum gas used off public highways. |

| Governing Law | This form is governed by Chapter 243 of the Hawaii Revised Statutes (HRS). |

| Who Needs It? | Every purchaser of diesel oil or liquefied petroleum gas for off-highway use must furnish this certificate to the distributor. |

| Exceptions | An Exemption Certificate is not required if liquefied petroleum gas is used solely for heating purposes. |

| Filing Frequency | The certificate must be provided annually or whenever there is a change in the intended use of the fuel. |

| Consequences of Non-Compliance | If the certificate is not provided, taxes will be imposed as if the fuel is used on public highways. |

| Tax Refunds | Purchasers can obtain refunds for taxes paid if they can prove the fuel was used off public highways. |

| Multiple Fuels | Separate Exemption Certificates are required for diesel oil and liquefied petroleum gas if both are purchased for off-highway use. |

| Additional Statements | Purchasers must provide additional statements detailing the breakdown of fuel use if not used off public highways. |

| Liability for Misuse | Purchasers who misuse the certificate by using off-highway fuel on highways may incur additional taxes. |

Misconceptions about the Hawaii M 38 Form

Here are key takeaways about filling out and using the Hawaii M-38 form: