Free Hawaii N 289 Template

Free Hawaii N 289 Template

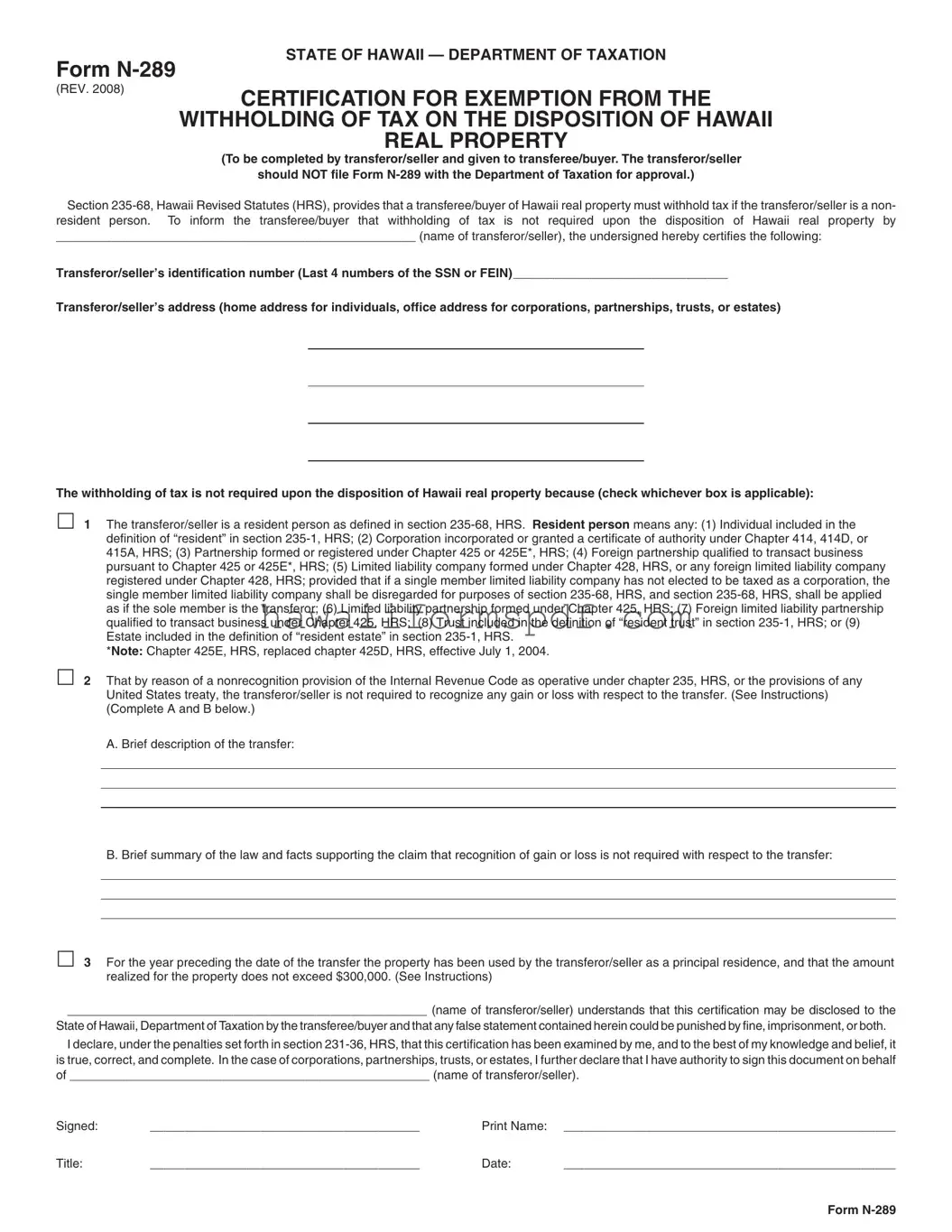

The Hawaii N-289 form plays a crucial role in real estate transactions within the state, specifically when it comes to tax withholding. This form is used to certify that the withholding of tax is not necessary when a transferor, or seller, disposes of Hawaii real property. It's essential for the seller to complete this form and provide it to the buyer, known as the transferee. The transferor must not submit the form to the Department of Taxation for approval. The form outlines several key exemptions from tax withholding, such as when the seller is a resident person, when a nonrecognition provision of the Internal Revenue Code applies, or when the property has been the seller's principal residence for the year prior to the transfer and the sale amount does not exceed $300,000. By filling out the form accurately, sellers can help ensure a smooth transaction while informing buyers of their tax obligations. It is important to note that providing false information on this form can lead to serious consequences, including fines or imprisonment. Understanding the purpose and requirements of the Hawaii N-289 form is vital for anyone involved in the sale of real property in Hawaii.

STATE OF HAWAII — DEPARTMENT OF TAXATION

Form

(REV. 2008)

CERTIFICATION FOR EXEMPTION FROM THE

WITHHOLDING OF TAX ON THE DISPOSITION OF HAWAII

REAL PROPERTY

(To be completed by transferor/seller and given to transferee/buyer. The transferor/seller should NOT file Form

Section

____________________________________________________ (name of transferor/seller), the undersigned hereby certifies the following:

Transferor/seller’s identification number (Last 4 numbers of the SSN or FEIN) _______________________________

Transferor/seller’s address (home address for individuals, office address for corporations, partnerships, trusts, or estates)

The withholding of tax is not required upon the disposition of Hawaii real property because (check whichever box is applicable):

1 The transferor/seller is a resident person as defined in section

*Note: Chapter 425E, HRS, replaced chapter 425D, HRS, effective July 1, 2004.

2 That by reason of a nonrecognition provision of the Internal Revenue Code as operative under chapter 235, HRS, or the provisions of any United States treaty, the transferor/seller is not required to recognize any gain or loss with respect to the transfer. (See Instructions) (Complete A and B below.)

A. Brief description of the transfer:

B. Brief summary of the law and facts supporting the claim that recognition of gain or loss is not required with respect to the transfer:

3 For the year preceding the date of the transfer the property has been used by the transferor/seller as a principal residence, and that the amount realized for the property does not exceed $300,000. (See Instructions)

____________________________________________________ (name of transferor/seller) understands that this certification may be disclosed to the

State of Hawaii, Department of Taxation by the transferee/buyer and that any false statement contained herein could be punished by fine, imprisonment, or both.

I declare, under the penalties set forth in section

Signed: |

_______________________________________ |

Print Name: |

________________________________________________ |

Title: |

_______________________________________ |

Date: |

________________________________________________ |

Form

INSTRUCTION |

STATE OF HAWAII — DEPARTMENT OF TAXATION |

FORM

(REV. 2008)

Instructions for Form

CERTIFICATION FOR EXEMPTION FROM THE WITHHOLDING OF TAX ON THE DISPOSITION OF HAWAII REAL PROPERTY

General Instructions

Purpose of Form

Use Form

Who Can Complete Form

The transferor/seller can complete Form

Where to Send Form

Form

Specific Instructions

At the top of Form

Check the applicable box to indicate the reason the withhold- ing of tax is not required upon the disposition of Hawaii real property.

Box number 1. Check box number 1 if the transferor/seller is a resident person as defined in section

Box number 2. Check box number 2 if by reason of a nonrecognition provision of the Internal Revenue Code as oper- ative under chapter 235, HRS, or the provisions of any United States treaty, the transferor/seller is not required to recognize any gain or loss with respect to the transfer. Complete sections A and B requesting a brief description of the transfer and a brief summary of the law and facts supporting the claim that recogni- tion of gain or loss is not required with respect to the transfer.

NOTE: If the withholding of tax is not required upon the dispo- sition of Hawaii real property because the disposition qualifies for the exclusion of gain from the sale of a principal residence under Internal Revenue Code section 121, check box number 2.

Box number 3. Check box number 3 if for the year preceding the date of the transfer the property has been used by the trans- feror/seller as a principal residence, and the amount realized for the property does not exceed $300,000. The "amount realized" means the sum of the cash paid, or to be paid (not including in- terest or original issue discount), the fair market value of other property transferred or to be transferred, and the amount of any liability assumed by the transferee/buyer or to which the Hawaii real property interest is subject to immediately before and after the transfer. Generally, the amount realized, for purposes of this withholding, is the sales or contract price.

NOTE: Although the withholding of tax may not be required upon the disposition of Hawaii real property, the trans- feror/seller is required under section

Signature

Form

Where to Get Information

Taxpayer Services Branch

P. O. Box 259

Honolulu, HI

Tel. No.:

Toll Free:

Completing the Hawaii N-289 form is an essential step for transferors or sellers of real property in Hawaii to inform the buyer that tax withholding is not required. After filling out the form, the transferor/seller should provide it to the buyer, who will keep it for their records. The transferor/seller does not need to file this form with the Department of Taxation.

Filling out the Hawaii N-289 form can be a straightforward process, but many make common mistakes that can lead to complications. One frequent error is failing to provide the correct identification number. This number must be the last four digits of the Social Security Number or the Federal Employer Identification Number. Leaving this blank or entering an incorrect number can delay processing and create unnecessary confusion.

Another mistake involves the transferor/seller's address. Individuals often provide an office address instead of a home address, or vice versa. This can lead to issues, especially if the property is owned by a corporation or partnership. Ensure that the address corresponds correctly to the type of entity involved in the transaction.

Many people also overlook the requirement to check the appropriate box indicating why tax withholding is not required. Each box corresponds to specific conditions, and failing to check any box can result in the form being rejected. Take the time to review each option and select the one that accurately reflects your situation.

In addition, when completing sections A and B, individuals sometimes provide vague descriptions or insufficient details. A brief description of the transfer and a clear summary of the law supporting the claim are essential. Ambiguities can lead to questions from the Department of Taxation, causing delays.

Another common oversight is related to the principal residence requirement. If the property has not been used as a principal residence for the year preceding the transfer, box three should not be checked. Misrepresenting this fact can lead to serious consequences, including penalties.

People often neglect to sign the form or fail to include the printed name and title where applicable. This might seem minor, but without a signature, the form is incomplete. Ensure that the form is signed by the correct individual, whether it be the transferor/seller or an authorized agent.

Some individuals mistakenly believe that they need to file the N-289 with the Department of Taxation. This is incorrect. The form should only be given to the transferee/buyer. Misunderstanding this requirement can lead to unnecessary filings and confusion.

Another issue arises when individuals do not keep a copy of the completed form. Retaining a copy is crucial for personal records and for any future inquiries regarding the transaction. Without a copy, it may be difficult to address any questions or disputes that arise later.

Finally, failing to understand the implications of false statements on the form can lead to severe penalties. Individuals must recognize that any inaccuracies can result in fines or imprisonment. It’s vital to ensure that all information provided is accurate and truthful.

When dealing with the Hawaii N-289 form, several other documents may also be necessary to ensure a smooth transaction involving the disposition of Hawaii real property. Each of these forms serves a specific purpose and can help clarify the tax obligations of the parties involved. Below is a list of commonly used forms that may accompany the Hawaii N-289.

Understanding these forms and their purposes can help facilitate a smoother transaction when selling or buying real estate in Hawaii. Always ensure that you have the correct documentation in place to meet all legal and tax obligations.

Bringing a Dog to Hawaii - The brochure shares complete care practices for maintaining your pet's well-being.

For those looking to complete their Texas Certificate of Insurance requirements, it’s important to access the necessary forms promptly, such as those available through Texas Documents, to ensure all plumbing operations run smoothly and comply with state regulations.

Form G-45 - The G 17 form reflects the regulatory framework of Hawaii's taxation system.

The Hawaii N-289 form is used to certify that the withholding of tax is not required when disposing of Hawaii real property. This applies if the transferor/seller is a resident person, if a nonrecognition provision of the Internal Revenue Code applies, or if the property has been used as a principal residence and the sale amount does not exceed $300,000.

The transferor/seller is responsible for completing the N-289 form. They must provide the form to the transferee/buyer but should not file it with the Department of Taxation.

At the top of the N-289 form, include the transferor/seller's name, the last four digits of their Social Security Number (or other identification number), and their address. If the transferor/seller is an individual without a Social Security Number, they should use their Individual Taxpayer Identification Number (ITIN).

Withholding tax is not required if:

"Amount realized" refers to the total cash paid, the fair market value of any other property transferred, and any liabilities assumed by the buyer. Generally, it is equivalent to the sales or contract price of the property.

If one or more, but not all, transferors provide a certification on Form N-289, the transferee/buyer must attach a copy of the form to Forms N-288 and N-288A when filing with the Department of Taxation.

The form must be signed by the transferor/seller, a responsible corporate officer, a member or general partner of a partnership, or a fiduciary of a trust or estate. An authorized agent with a power of attorney can also sign.

No, the transferor/seller should not file the N-289 form with the Department of Taxation. The transferee/buyer retains the form for their records.

For more information, you can contact the Taxpayer Services Branch at P.O. Box 259, Honolulu, HI 96809-0259. You can also call 808-587-4242 or toll-free at 1-800-222-3229.

| Fact Name | Fact Details |

|---|---|

| Form Purpose | Form N-289 certifies that the withholding of tax is not required on the sale of Hawaii real property. |

| Governing Law | The form is governed by Section 235-68 of the Hawaii Revised Statutes (HRS). |

| Who Completes the Form | The transferor or seller of the property must complete Form N-289. |

| Filing Instructions | The transferor/seller should provide the form to the transferee/buyer but should not file it with the Department of Taxation. |

| Exemption Criteria | Withholding is not required if the transferor/seller is a resident person or meets specific IRS nonrecognition provisions. |

| Principal Residence Rule | If the property has been used as a principal residence and sold for under $300,000, withholding is also not required. |

| Signature Requirements | The form must be signed by the transferor/seller or an authorized representative, such as a corporate officer or trustee. |

| Disclosure | The certification may be disclosed to the State of Hawaii, and false statements can lead to penalties. |

Filling out the Hawaii N-289 form can be straightforward if you keep a few key points in mind. Here are some essential takeaways to help guide you through the process:

By keeping these points in mind, you can navigate the Hawaii N-289 form with confidence and ensure that all necessary information is accurately provided.