Free Hawaii Promissory Note Form

Free Hawaii Promissory Note Form

The Hawaii Promissory Note form serves as a crucial financial document for individuals and businesses engaging in lending and borrowing transactions within the state. This form outlines the borrower's promise to repay a specific amount of money to the lender, detailing the terms of the loan, including interest rates, payment schedules, and maturity dates. It is designed to protect both parties by clearly stating their rights and obligations. The document typically includes essential elements such as the principal amount, the interest rate, and any collateral involved in the transaction. Additionally, the form may specify the consequences of default, ensuring that all parties understand the implications of failing to meet the agreed-upon terms. By providing a structured approach to personal and commercial loans, the Hawaii Promissory Note form facilitates trust and accountability between lenders and borrowers, making it an essential tool in the financial landscape of the state.

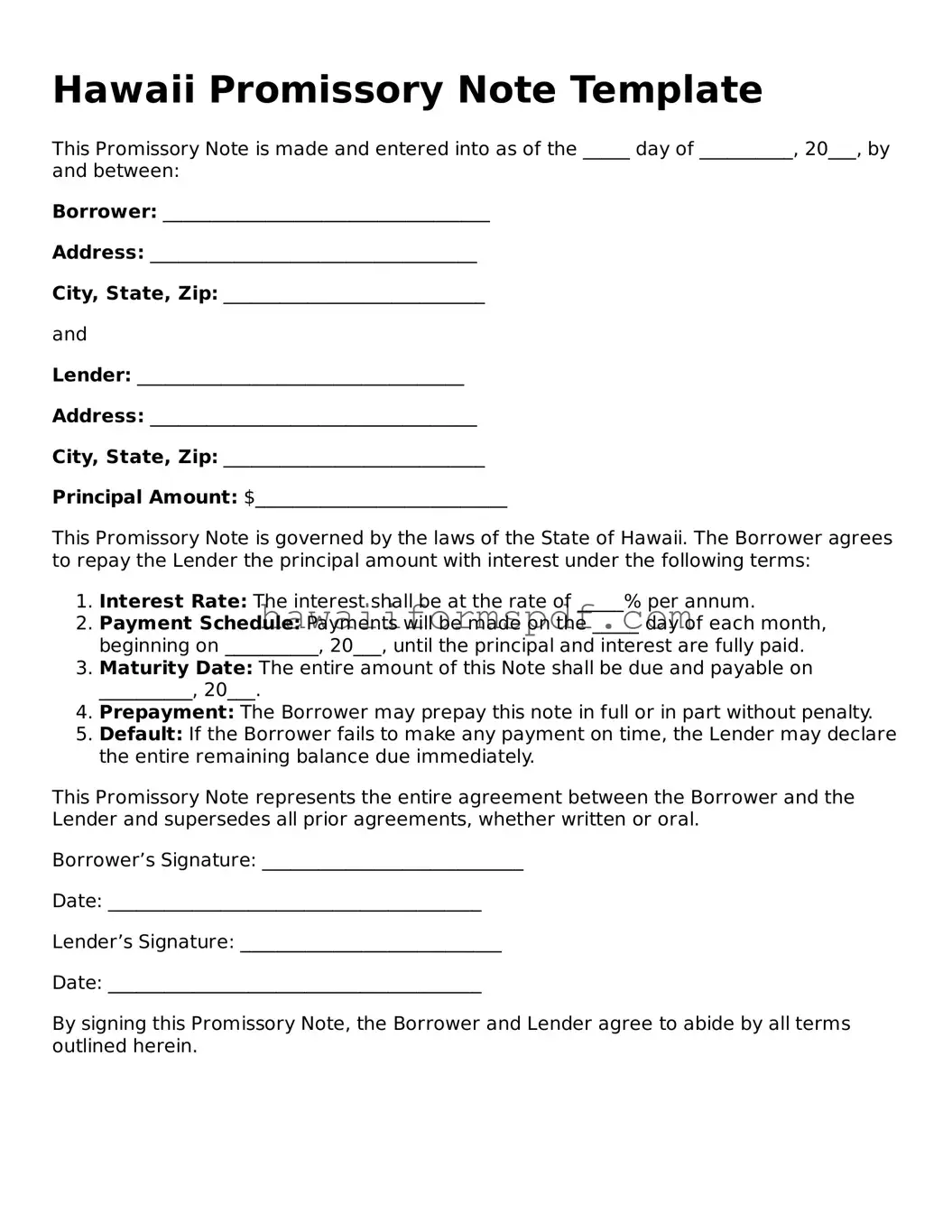

Hawaii Promissory Note Template

This Promissory Note is made and entered into as of the _____ day of __________, 20___, by and between:

Borrower: ___________________________________

Address: ___________________________________

City, State, Zip: ____________________________

and

Lender: ___________________________________

Address: ___________________________________

City, State, Zip: ____________________________

Principal Amount: $___________________________

This Promissory Note is governed by the laws of the State of Hawaii. The Borrower agrees to repay the Lender the principal amount with interest under the following terms:

This Promissory Note represents the entire agreement between the Borrower and the Lender and supersedes all prior agreements, whether written or oral.

Borrower’s Signature: ____________________________

Date: ________________________________________

Lender’s Signature: ____________________________

Date: ________________________________________

By signing this Promissory Note, the Borrower and Lender agree to abide by all terms outlined herein.

After obtaining the Hawaii Promissory Note form, it’s essential to complete it accurately to ensure clarity and enforceability. Follow these steps to fill out the form correctly.

Once the form is filled out, it’s advisable to keep copies for both parties. This ensures that everyone has a record of the agreement and its terms. Proper documentation can help prevent misunderstandings in the future.

Filling out a Hawaii Promissory Note form requires careful attention to detail. One common mistake people make is failing to include the correct names of the parties involved. It is crucial to ensure that the borrower and lender's full legal names are accurately stated. Omitting or misspelling a name can lead to complications in enforcing the note.

Another frequent error is not specifying the loan amount clearly. This figure should be written in both numerical and written form to avoid any ambiguity. For instance, writing “$10,000” and “Ten Thousand Dollars” helps prevent misunderstandings about the loan amount.

People often overlook the importance of the interest rate. It must be clearly defined, including whether it is fixed or variable. If the interest rate is not specified, it can lead to disputes later on regarding how much the borrower owes.

Additionally, many individuals forget to include the repayment terms. This section should outline how and when the borrower will repay the loan. Without clear terms, confusion may arise, leading to potential defaults and legal issues.

Another mistake involves not dating the document. A promissory note should always include the date it is signed. This date is essential for tracking the timeline of the loan and establishing when payments are due.

Some people neglect to have the document notarized. While not always required, notarization can add an extra layer of authenticity and can be crucial if the note needs to be enforced in court.

Lastly, failing to keep a copy of the signed promissory note is a significant oversight. Both parties should retain a copy for their records. This ensures that everyone is aware of the terms and can refer back to the document if necessary.

When using a Hawaii Promissory Note, there are several other documents that may be relevant to the transaction. Each of these documents serves a specific purpose and helps ensure that both parties are protected throughout the lending process. Here are some common forms that often accompany a Promissory Note:

Understanding these accompanying documents can help both parties navigate the lending process more smoothly. Each document plays a vital role in ensuring clarity and protection for everyone involved.

Non Compete Agreement Hawaii - This form often includes considerations for remote work arrangements.

The process of obtaining the Arizona Board of Nursing License is not only vital for aspiring nurses but also serves as a foundational step in ensuring a thorough understanding of the nursing regulations within the state. Those interested in navigating this complex landscape can reference the Arizona Board of Nursing License form, which encompasses essential information regarding licensure requirements and practices. To enhance your understanding and streamline your application process, you can learn more about the document that outlines everything you need to know.

Hawaii Power of Attorney - Consideration of state-specific laws is important, as requirements for this document can vary significantly.

A Hawaii Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender under agreed-upon terms. This note serves as a written record of the loan agreement, detailing important elements such as the loan amount, interest rate, repayment schedule, and any consequences for defaulting on the loan.

Promissory Notes are commonly used by individuals, businesses, and organizations in Hawaii. They may be utilized in various situations, including personal loans between friends or family members, business loans, or real estate transactions. Essentially, anyone who needs to borrow or lend money may find this document useful for formalizing their agreement.

A well-drafted Promissory Note should include the following key elements:

While both documents serve similar purposes, a Promissory Note is generally simpler and focuses solely on the borrower's promise to repay the loan. A loan agreement, on the other hand, may include more detailed terms and conditions, such as collateral, warranties, and additional obligations of both parties. In essence, a Promissory Note is a subset of a broader loan agreement.

It is not strictly necessary to hire a lawyer to create a Promissory Note in Hawaii, as many templates and resources are available online. However, consulting with a legal professional can be beneficial, especially for larger loans or complex agreements. A lawyer can ensure that the document complies with state laws and adequately protects your interests.

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is important to document any modifications in writing and have both parties sign the updated agreement. This helps prevent misunderstandings and provides a clear record of the new terms.

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. The specific consequences should be outlined in the Promissory Note. Common actions may include:

It's essential for both parties to understand these terms before entering into the agreement.

Yes, a properly executed Promissory Note is generally enforceable in Hawaii, provided it meets the legal requirements set forth by state law. To ensure enforceability, the document should be clear, signed by both parties, and contain all necessary elements. If disputes arise, having a well-drafted Promissory Note can significantly aid in legal proceedings.

| Fact Name | Details |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a certain time. |

| Governing Law | The Hawaii Promissory Note is governed by the Hawaii Uniform Commercial Code (UCC), specifically under Chapter 490. |

| Types | Promissory notes can be secured or unsecured, depending on whether collateral is involved. |

| Interest Rates | The interest rate can be fixed or variable, and it should be clearly stated in the note. |

| Signatures | The borrower must sign the note for it to be legally binding; the lender’s signature is not always required. |

| Enforceability | A properly executed promissory note is enforceable in court, provided it meets all legal requirements. |

Understanding the Hawaii Promissory Note form is essential for anyone involved in lending or borrowing money in the state. However, several misconceptions can lead to confusion. Here are six common misunderstandings:

By addressing these misconceptions, individuals can approach the Hawaii Promissory Note with a clearer understanding, ensuring a smoother lending process.

Filling out and using the Hawaii Promissory Note form involves several important considerations. Here are key takeaways to keep in mind:

By following these guidelines, individuals can ensure that their promissory note is properly filled out and legally enforceable.